UPM-Kymmenen poised to deliver growth?

UPM-Kymmenen poised to deliver growth?

Beautiful simple business with the best management in the whole Europe.

This is just a quick look at the UPM-Kymmenen financial results for 2022. No financial advice. What are your country’s sleeping value companies? Those that sit right under our noses and don’t make many headlines? Just focusing on making shareholders happy.

Why on earth would I be interested in Finnish pulp & paper company? Simply to have some diversification. Owning 40-100 different stocks is not diversification. It is assets that matter in the end (more on this on some other piece). I have to own at least one Finnish stock, and UPM is the only one I am willing to own at this time:

Simple business

I want to own this company forever

No stress

Best management (Even I could bully 95% of other Finnish companies’ CEO and boards of directors and tell them you are fucking idiots, they just are.) In front of these guys, I would feel humbled and embarrassed like a little kid after being naughty…

Aggressive dividend policy & stock buyback program. The new dividend policy aims for 50% of EPS.

Great MOAT

A little bit of that “green energy” hype, but this is not the stock for that play, even though these “green deals” etc are total scams, it does not mean the stocks/raw materials don’t have any legs, these will run hard, and we will focus on these too and find them ten baggers in this “green deal” decade.

UPM YEAR 2022 Financials (from 2022 q4 report)

Simple business.

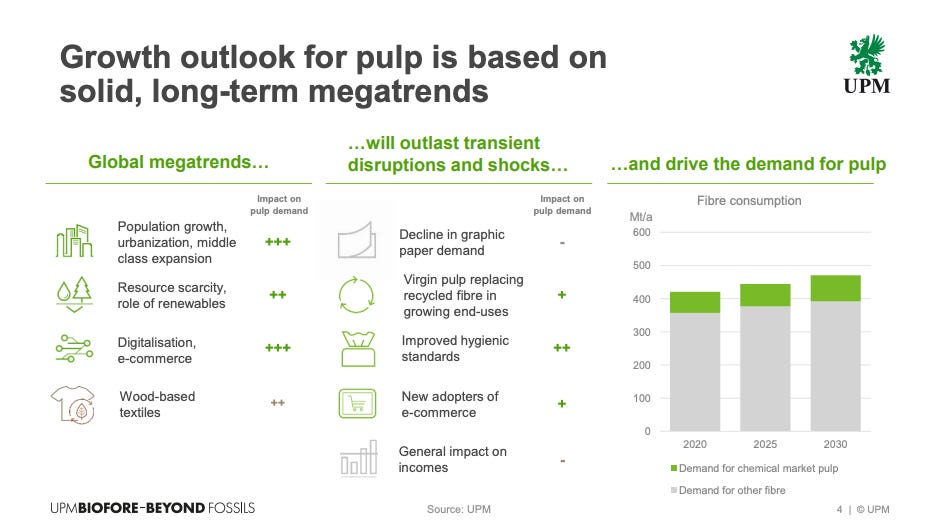

We want to focus on the revenue side, is it shrinking? growing? staying the same? In general, pulp is needed for various products such as paper, and packaging materials. Nothing exciting, simple! Volumes are down, and demand is slowing, though… 2022 was exceptionally good, and market conditions were favoring the likes of UPM massively.

→ Solid demand no matter what.

Yeah, this is not a business that will disrupt the world, but 150 years of forest industry at UPM. They know how to run this.

Big investments in Uruguay, starting to run in late Q1 2023.

The investment will grow UPM's current pulp capacity by more than 50%

→ Scale the business

→ Grow future earnings

→ Secured around 500,000 hectares of plantations

Again they have 150-year track record in the forest industry and also +30y from Uruguay, so I am pretty confident they can run this investment profitably.

They also have a very nice energy business. UPM’s power generation capacity consists of hydropower, nuclear power, and thermal power. “Carbon-free” and the second largest producer in Finland currently.

→ OL3 starting finally this year? (UPM owns part of it) Big nuclear plant. Will grow UPM Energy’s carbon-free electricity generation by nearly 50%

Simply awesome and pretty nice to own a piece of this too.

COSTS???

Why you don’t analyze the costs??? Even though this is a highly cost-intensive business?

Again this is an extremely well-managed business, and very refreshing to read the financial results of an actual business with value.

+500 000 acres of wood supply (Uruguay)

Second biggest energy producer in Finland

Biggest risks:

Bottlenecks in global logistics.

(Normalization of supply chains?) Did everybody stock too much?

Finnish government (socialist country) also European Union.

Taxes? Regulation? Windfall tax?

Even the greatest companies can’t affect this dark development in Europe.

Future potential?

The core business has solid growth and demand, everything else is just a bonus.

New business in wood-based biochemicals? Again 150-year track record in the forest industry, they are leading the way in innovation when it comes to wood-based products. UPM operates currently one biorefinery in Finland. The new one will be up and running in Germany in late 2023.

The biorefinery will produce a range of 100% wood-based biochemicals, which will enable a switch from fossil raw materials to sustainable alternatives in various consumer-driven end-uses. The investment opens up totally new markets for UPM, with large growth potential for the future.

If there are huge innovations in wood-based chemicals or whatever, UPM will play a big part in it no matter what.

→ Growing demand for sustainable solutions - Anything related to wood - UPM?

Negatives

Management is retiring…

Jussi Pesonen retires 2024

Björn Wahlroos las year as Chair.

This is pretty big, but I am confident they will leave the company in “good hands,” on the plus side, the business is so simple and beautiful that even average management cannot destroy this. Keep an eye out if Pesonen and Wahlroos start to dump their papers then it’s time to revalue. I think they also want to own UPM forever, if not, don’t touch this.

Does not have “supervalue” multi-bagger potential.

The core business is still somewhat cyclical, but excellent management and the new Uruguay plant will make earnings more stable?

Located in Finland, prone to weird government decisions, future taxation? What about European Union decisions?

Does it get huge subsidies from the government? German companies get the biggest… Finland will be a big loser in this “deglobalization” and subsidy game, but this should not have that big impact on UPM, but is still a risk.

Conclusion

Passive income while I sleep? I like to have a few dividend stocks. UPM is an extremely solid company that can grow to a real dividend payout machine (it is already pretty nice).

Valuation is somewhat high, and we might get good buying opportunities soon.

Did customers stock too much during 2022?

Will Uruguay start to print late q1 2023?

The stock ran pretty nicely already from the summer of 2022.

Long term outlook still looks promising.